Historic Mortgage Rates by Decade: How Today’s Rates Compare

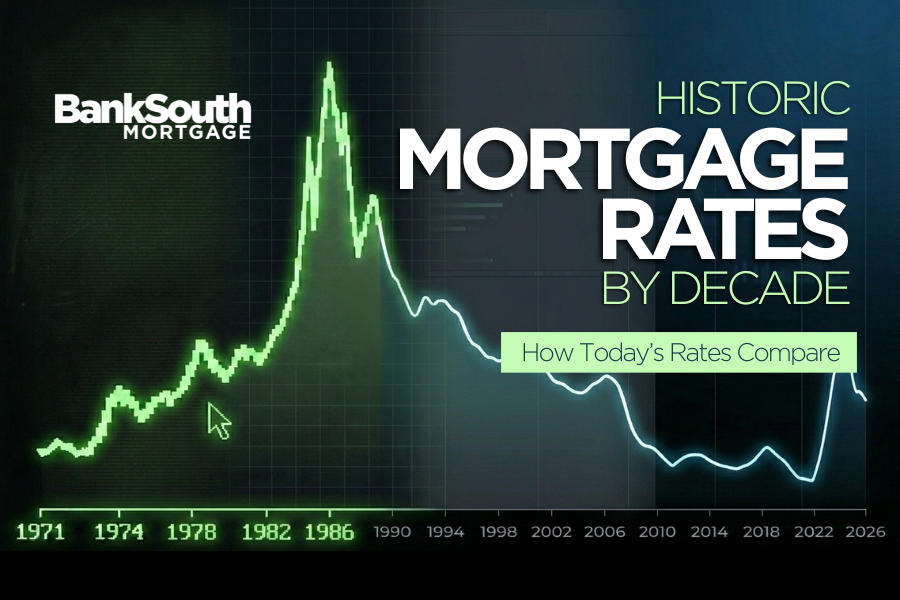

Today’s mortgage rates are higher than the record-low rates many buyers remember from 2020 and 2021, but they remain far below some of the highest mortgage rate environments in modern history. According to Freddie Mac’s Primary Mortgage Market Survey®, the 30-year fixed mortgage rate averaged 6.37% for the week of May 7, 2026. In comparison, mortgage rates climbed above 16% in the early 1980s.

That historical perspective matters. When buyers only compare today’s rates to the unusually low rates of recent years, it can make the current market feel more discouraging than the bigger picture suggests. Mortgage rates have always moved in cycles, and homeownership has always been a long-term financial decision.

Why Mortgage Rate History Matters for Today’s Buyers

Mortgage rates influence monthly payments, affordability, and buying power. But they are only one part of the homebuying decision.

A lower rate can help reduce a monthly payment, but waiting for rates to fall can also come with tradeoffs, including rising home prices, more buyer competition, fewer seller concessions, or limited inventory. A higher rate environment may feel challenging, but it can also create opportunities for buyers who are prepared, informed, and guided by a trusted mortgage advisor.

Understanding historical mortgage rates helps buyers see today’s market with more clarity and less fear.

How Today’s Mortgage Rates Compare to the Past

Mortgage rates have changed significantly over the last five decades:

- In the 1970s, rates began rising as inflation increased.

- In the early 1980s, mortgage rates reached historic highs above 16%.

- In the 1990s and early 2000s, rates gradually moved lower.

- In 2020 and 2021, rates reached historic lows.

- Today, rates are higher than recent lows but still well below the peaks of previous decades.

The key takeaway: today’s rates may feel high compared to the last few years, but they are not historically high when viewed across the full timeline of modern mortgage lending.

What Higher Mortgage Rates Mean for Homebuyers

Higher rates can affect affordability, but they do not automatically mean buying a home is out of reach. Many buyers are still moving forward by focusing on strategy instead of headlines.

Today’s buyers may benefit from exploring options such as:

- Seller concessions

- Temporary rate buydowns

- Adjustable-rate mortgage options, when appropriate

- Refinancing opportunities if rates improve later

- Loan programs that better align with their financial goals

- A purchase price and payment range that supports long-term comfort

The right mortgage strategy depends on your income, credit, savings, goals, timeline, and comfort level. That’s why personalized guidance matters.

Should You Wait for Mortgage Rates to Drop?

There is no one-size-fits-all answer. Some buyers may choose to wait, while others may find that buying now makes sense based on their life stage, local market conditions, financial readiness, and long-term plans.

Instead of asking, “Are rates too high?” a more helpful question may be:

“Can I find a home and mortgage payment that fits my goals right now?”

If the answer is yes, today’s market may still offer opportunity. If the answer is not yet, a mortgage advisor can help you build a plan so you are prepared when the timing feels right.

The Bigger Picture: Homeownership Is a Long-Term Strategy

Mortgage rates rise and fall, but the long-term benefits of homeownership can include stability, equity growth, and the ability to build wealth over time. The goal is not to perfectly time the market. The goal is to make an informed decision that supports your life and financial future.

At BankSouth Mortgage, our team helps buyers understand their options, compare scenarios, and move forward with confidence. Whether you are buying your first home, moving into your next home, or exploring whether now is the right time to refinance, we are here to help make the mortgage process clearer, simpler, and more personal.

Ready to Talk Through Your Options?

If you are wondering how today’s mortgage rates affect your homebuying plans, connect with a BankSouth Mortgage loan officer. We can help you review your goals, understand your buying power, and create a mortgage strategy that fits your needs.

Leave a Reply

Want to join the discussion?Feel free to contribute!