Why Aren’t ARMs More Popular in This Increasing Interest Rate Environment?

The answer to this question involves an intricate dance between risk, time, and interest—all depicted in a single graph: the Treasury Yield Curve.

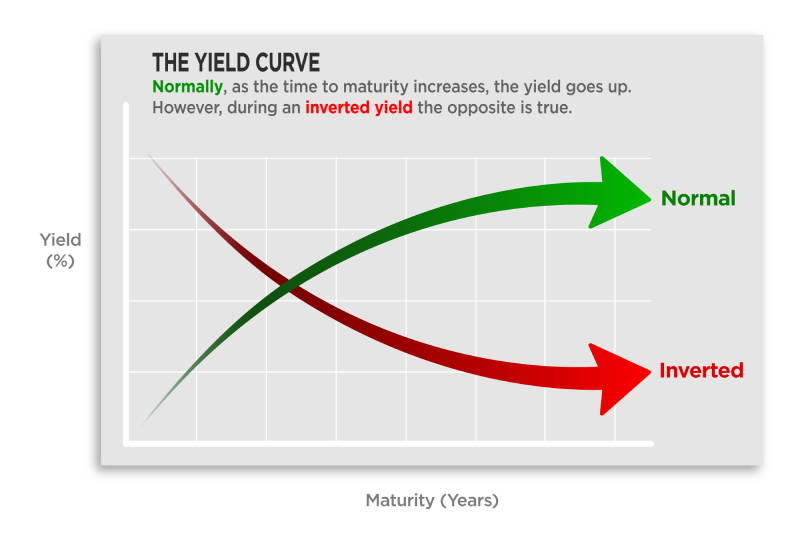

What is a Treasury Yield Curve?

This is a graph that visually represents the annual interest rate that the U.S. government pays on its debt obligations. In other words, it tells investors the annual return they can expect from holding a government security with a given maturity, showing us the relationship between interest rates.

Usually, this line goes up, meaning if you borrow money for a longer time, you pay more in interest because lending money for a longer time is usually riskier.

In our current market, we have an inverted Treasury Yield Curve. This means you pay more to borrow money for a shorter time, which is unusual and can signal that people are worried about the economy’s future.

What causes an Inverted Treasury Yield Curve?

It has everything to do with investors – investors in mortgages and investors in Treasury Bonds.

Mortgage companies sell mortgages to investors as mortgage-backed securities. This process allows them to get more funds to offer more loans to borrowers. Investors get a return on their investment through the interest paid on those mortgages. When investors buy Treasury bonds, they are essentially lending money to the government. The government uses these funds for various expenditures, and in return, it pays interest to the bondholders. Treasury bonds are considered low-risk investments compared to stocks or other securities.

How are these investments related? The yield, or the interest rate on Treasury bonds, reflects the general level of risk in the financial market. When investors feel uncertain about the economy, they tend to prefer safer investments like Treasury bonds over riskier ones like stocks or even mortgage-backed securities. The yields on Treasury bonds serve as a benchmark for various interest rates, including those on mortgages. If the yield on long-term Treasury bonds is low, it can lead to lower interest rates on long-term fixed-rate mortgages, making them more attractive to borrowers compared to adjustable-rate mortgages, and vice versa.

An inverted Treasury yield curve occurs when the interest rates on short-term Treasury bonds are higher than the interest rates on long-term Treasury bonds. Here’s a simplified explanation of what causes an inverted Treasury yield curve:

Central Bank Policy:

- Interest Rate Increases: When a central bank, like the U.S. Federal Reserve, raises short-term interest rates to combat inflation or stabilize the currency, it can cause short-term yields to surpass long-term yields.

- Monetary Tightening: Central banks might reduce the supply of money in the economy, making short-term credit more expensive, contributing to yield curve inversion.

Investor Behavior and Market Sentiment:

- Flight to Quality: Investors might prefer long-term bonds as safe-haven assets in times of economic uncertainty, driving up their prices and reducing their yields.

- Recession Expectations: If investors expect an economic downturn, they might flock to the perceived safety of long-term bonds, accepting lower yields for the promise of capital preservation.

Economic Indicators and Outlook:

- Expectation of Lower Future Growth: Pessimistic economic forecasts can lead to a higher demand for long-term bonds, as investors seek stable returns, pushing their yields below short-term yields.

- Inflation Expectations: If investors expect lower inflation in the future, the real return on long-term bonds seems more attractive, leading to higher demand and lower yields on these bonds compared to short-term bonds.

How does an Inverted Treasury Yield Curve impact investors?

When the Treasury Yield curve is inverted, it often signals that investors are worried about the future of the economy. Investors typically find themselves leaning towards safer, long-term investments like government bonds, even if they offer lower interest. This rush towards safety can reduce the returns they get on these safe investments because the high demand for long-term bonds raises their prices but lowers their yields or interest rates.

How does an Inverted Treasury Yield Curve impact borrowers?

If an investor cannot create a profitable and appealing ARM deal due to the current market scenario, then the borrowers are left with ARM options that are less advantageous compared to a 30-year Fixed-Rate Mortgage.

An inverted yield curve for borrowers looking to get a mortgage or a loan can mean they might find that the interest rates for short-term loans are unusually high compared to long-term loans. This situation could make fixed-rate long-term loans more attractive to borrowers seeking stability in their payment plans, even if typically, they might have considered adjustable-rate or shorter-term loans due to initially lower interest rates. In this environment, borrowers might lean more towards locking in a rate with a long-term fixed-rate loan to avoid the uncertainty and higher costs associated with short-term borrowing.

In the current market, a unique scenario is unfolding where the rates on Adjustable-Rate Mortgages (ARMs) could potentially surpass the rates of 30-year Fixed-Rate Mortgages (FRMs) at similar price points due to unfavorable market conditions and investor preferences. This situation leaves borrowers with Fixed-Rate Mortgages as the most sensible choice, offering stability and value, whereas Adjustable-Rate Mortgages may not present any distinct advantage, potentially costing more in the long run.

In summary, the current preference for Fixed-Rate Mortgages over ARMs is mostly due to the inverted Treasury Yield Curve, which shows a unique dance between risk, time, and interest. This curve helps us see why, in times of economic uncertainty, steady and predictable payments like those from Fixed-Rate Mortgages are often the wise choice for borrowers. At BankSouth Mortgage, we’re here to help you navigate through these choices and find what works best for you. Reach out to us for simple, clear advice, and make your mortgage decisions with confidence!

Leave a Reply

Want to join the discussion?Feel free to contribute!