Step-by-step VA Loan Process and Highlights

Are you active or retired military, or even a surviving military spouse? Good news! You may qualify for a VA loan! A VA loan is a type of loan that is guaranteed by the U.S. government to help active or retired military and their spouses obtain the dream of homeownership. There are several advantages to getting a VA-backed loan. Up to 100% financing, no monthly mortgage insurance, fixed and adjustable rates are available, among other perks. Explore other highlights as well as the 8 simple steps to a VA loan at BankSouth Mortgage.

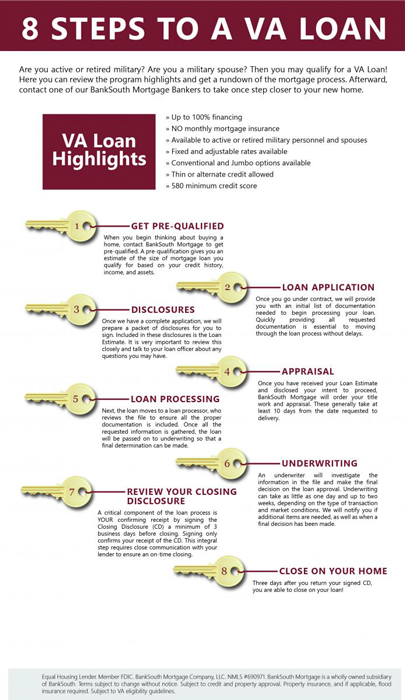

VA Loan Highlights:

- Up to 100% financing

- No monthly mortgage insurance required.

- Available to active or retired military personnel, and eligible surviving spouses of the military

- Fixed and adjustable rates are available

- Conventional and conforming and non-conforming Jumbo loan options available

- 620 minimum credit score is required

Step 1: Get prequalified

When you begin thinking about buying a home, contact BankSouth Mortgage to get prequalified. A pre-qualification gives you an estimate of the size of mortgage loan you qualify for based on your credit history, income, and assets.

Step 2: Apply for your VA loan

Once you get under contract, we will provide you with an initial list of documents that are needed to begin processing your loan. Quickly providing all of the requested documentation is essential to moving through the loan process without delays.

Step 3: Disclosures

Once we have a complete application, we will prepare a packet of disclosures for you to sign. Included in these disclosures is the Loan Estimate. It is very important to review this closely and talk to your loan officer about any questions you may have.

Step 4: Appraisal

Once you have received your Loan Estimate and disclosed your intent to proceed, BankSouth Mortgage will order your title work and appraisal. These generally take at least 10 days from the date requested to deliver.

Step 5: Loan processing

Next, the loan moves to a loan processor, who reviews the file to ensure all the proper documentation is included. Once all the requested information is gathered, the loan will be passed on to underwriting so that a final determination can be made.

Step 6: Underwriting

An underwriter will review the information in the file and make the final decision on the loan approval. Underwriting can take as little as 24-48 hours depending on the type of transaction and market conditions. We will notify you if additional items are needed, as well as when a final decision has been made.

Step 7: Review your closing disclosure

A critical component of the loan process is YOUR confirming receipt by signing the Closing Disclosure (CD) a minimum of 3 business days before closing. Signing only confirms your receipt of the CD. This integral step requires close communication with your lender to ensure an on-time closing.

Step 8: Close on your home

Three days after you return your signed CD, you can close on your home loan! Depending on the amount due at closing, you may need to send a wire to the closing attorney. At the closing, you and the seller will be required to sign the final loan closing documents. After the closing documents are signed, BankSouth Mortgage will wire funds for the amount of the loan to the closing agent. The closing agent will disperse the funds. The deed that transfers the title from the seller to you will be sent to the county in which the home is located to be recorded. You will receive the original deed once it has been recorded along with your owner’s title insurance policy if you purchased insurance at closing.

VA-backed loans were designed to offer veterans and their spouses an easy way to achieve homeownership. Learn more about the VA requirements for obtaining a VA-backed loan at the Veteran Affairs website and our VA loan product page.

See how much home you can afford today. Get your fast preapproval today and contact one of our helpful Mortgage Bankers.

Leave a Reply

Want to join the discussion?Feel free to contribute!